eXp Realty has been focused on innovating and supporting agents in a virtual world since the very beginning. That’s why the brokerage has built its foundation on a state-of-the-art online platform to eliminate the traditional brick-and-mortar offices in favor of a cloud-based brokerage. That way, eXp can offer agents equal opportunity to build true wealth through virtually limitless earning potential. Every other real estate broker out there allows you to build one single income stream that comes from trading your time for money. Therefore, as soon as you stop showing properties all day long or stop picking up the phone late at night, you will stop receiving income. With eXp, you have most advantageous capped commission structure to build a successful real estate career then add in a passive income stream through revenue sharing program and become shareholders at eXp Realty in a variety of ways.

In this article, we will cover the following:

- eXp Commission – Equal Opportunity

- Transaction Fees

- Revenue Share

- eXp Stock Ownership

- Other Fees

- ICON program

eXp Realty Commission: Every Agent Has the Same Commission Structure at eXp

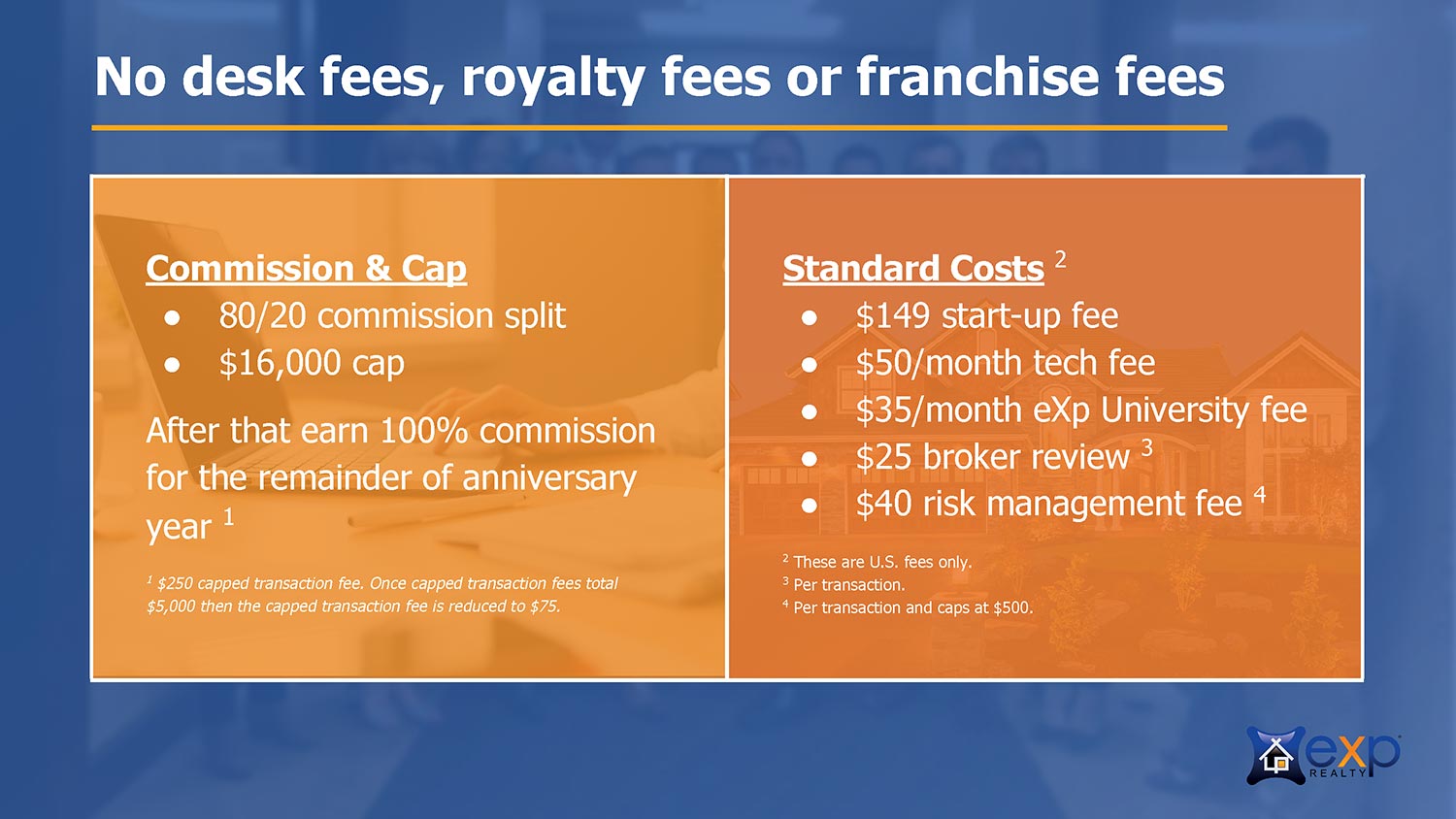

Unlike traditional brokerages where commissions are variable and often depend on an agent’s negotiating skills, production or relationships, all agents at eXp get the same commission structure: 80/20 with a $16,000 cap. Team members are eligible for one-half to a one-quarter cap, based on team performance.

That means agents at eXp keep 80% of the commission earned until they have paid a total of $16,000. After that, the agent keeps the entire commission (100%) for the duration of their anniversary year. There are no franchise or royalty fees charged at eXp Realty.

Transactional fees, charged only for closed sales, cover the broker review ($25) and risk management fee ($40) together capped at $500 per year.

See examples below for how commissions and costs break down.

The risk management fee caps at $500 and then goes to $0. The capped transaction fee reduces to $75 per transaction after $5,000 has been paid.

Example 1: Commission and fees for a $350,000 closing with 3% commission for an agent who has not reached the $16,000 cap:

Gross Commission = $10,500

- Deduct eXp Company Dollar = $2,100 (20%)

- Deduct Broker/Risk Fees = $65

Agent Net Commission = $8,335

Example 2: Commission and fees for a $350,000 closing with 3% commission for an agent who has reached the $16,000 cap:

Gross Commission = $10,500

- Deduct eXp Company Dollar = $0

- Deduct Capped Transaction Fee = $250

- Deduct Broker/Risk Fees = $65

Agent Net Commission = $10,185

eXp Realty Transaction Fees

After a real estate agent caps, they go to 100 percent and only pay $250 per transaction. If an agent pays in $5,000 in transaction fees after capping, they will move to a $75 per transaction fee for the remainder of the anniversary year.

For example, let’s say you sell 60 homes in one year with an average commission amount of $6,000 per transaction. Here is how your eXp Realty commission split would work out:

- Transactions 1-14 would be on an 80/20 split with NO transaction fee.

- Transactions 15-34 would be on a 100/0 split with a $250 transaction fee.

Transactions 35-60 would be on a 100/0 split with a $75 transaction fee.

To explain, you would cap on your 14th transaction ($6,000 x 14 transactions = $84,000). Transactions 15-34 would all be at $250/per transaction totaling $5,000. Transactions 35-60 would be at $75 per transaction.

eXp Revenue Share: Agents Earn Revenue Share Through Sponsored Agents

Perhaps one of the most exciting, yet misunderstood benefits at eXp is revenue share. The revenue share opportunity is simply when an agent joins eXp and names an active eXp agent as their “sponsor.” The sponsor is the eXp agent who was most influential in the new agent’s decision to join eXp.

Once the new agent begins closing on transactions, the sponsor receives a percentage of the company dollar (revenue) from the sales activity of their sponsored agent. It is based on gross commission income (GCI), and is dynamically calculated and paid monthly.

This is a different concept than profit-sharing, in which certain brokerages share company profits with agents after all expenses have been subtracted from revenue. That includes costs such as rent, insurance, utilities, staff salaries, and other costly overhead charges. In a profit-share model, it often happens that a sponsored agent is productive but the office or franchise is not profitable, resulting in minimal or zero profit-share.

eXp Stock: eXp Agents Can Acquire Stock in a Variety of Ways

The third unique form of compensation for agents at eXp is becoming a shareholder with the company. eXp Realty agents are awarded or can earn shares of stock in eXp World Holdings (eXp Realty’s parent company) after certain milestones are reached, including:

- Closing on the first transaction as an eXp Realty agent ($200 stock award)

- The first closed transaction by any agent they have sponsored ($400 stock award)

- Reaching the annual cap ($400 stock award)

- Reaching ICON Agent status ($16,000 stock award)

- Agents can also elect to receive up to 5% of their commissions from each closed sale in the form of eXp stock at a 10% discount through the Agent Equity Program.

Other eXp Fees

eXp Realty fees consist of monthly and transaction fees. I’ll cover each in more detail below.

eXp Realty does not charge a desk fee, royalty fee, or franchise fee. Also, there are no minimum production or attraction requirements. So long as you stay current on your $85 monthly fee and all state licensing requirements you can remain licensed at eXp Realty.

Risk Management Fee (Errors & Omissions)

Many agents are familiar with the term errors and omissions. At eXp Realty, we call this the risk management fee. The risk management fee varies by country, but in the US, it is $40 per transaction.

Once a real estate agent hits $500 in risk management fees paid for the year, the agent will no longer pay risk management fees for the remainder of the anniversary year.

Broker Review Fee

All US agents pay a $25 per transaction broker review fee.

This fee does not cap.

eXp Realty Mentor Fees

Agents who’ve completed less than three transactions in their current market will be enrolled in the eXp Realty’s mentor program. Agents in the mentor program are assigned a certified mentor who will help assist with the agent’s first three transactions at eXp Realty.

Mentees pay an additional 20 percent split on these first three transactions which pays the mentor and mentor program (which consists of additional training modules for the mentee).

Once the mentee closes three transactions with eXp Realty, they graduate from the mentor program and are not subject to the additional 20 percent commission split.

eXp Realty Seller Fees

eXp Realty does not charge any additional fees to clients. Agents can determine their commission rate and any additional fees to their clients. However, whatever rate and fees that are charged to the client are then split with eXp Realty at the typical commission split.

If an agent wishes to discount their commission rate and that agent has not reached their commission cap, the minimum transaction split to eXp Realty is $500. Therefore, an agent can reduce their commission completely to $0 to the client but the agent would then be responsible to pay eXp Realty $500 for that transaction, plus the broker review and risk management fee.

eXp Realty Personal Deals

At eXp Realty, agents can complete three personal transactions per year without paying the 20 percent split to eXp Realty.

Agents are only responsible to pay a $250 transaction fee, $40 risk management fee, and $25 broker review fee for the personal deal.

A personal transaction consists of only the deals for which the eXp Realty agent is personally on the contract.

Commission Split and Fees Example on 60 Transaction for the Year

Their total eXp Realty Commission Split paid for the year would equal:

- $16,000 – Cap

- $5,000 – $250 Transaction Fees

- $1,875 – $75 Transaction Fees

- $500 – Risk Management Fees

- $1,500 – Broker Review Fees

- $24,875 – Total eXp Realty Commission Split Fees

How would you like to earn $16,000 of those fees back? Read below about the ICON agent program at eXp Realty and see how you can do just that.

$500,000 Annual Gross Commission Income Plus ICON Qualifying Fee

The second way you could qualify to become an ICON agent is by achieving an “Annual gross commission income of $500,000 or more with a minimum of 10 closed transactions and payment of an “ICON Qualifying Fee.” This fee is equal to $5,000 less capped transaction fees paid during the same anniversary year.

The last part of becoming an ICON agent is to” Demonstrate company culture by giving back by teaching a class, serving on a panel, or serving on a committee. Also, an ICON agent must have a willingness to promote eXp Realty within their community.”

That’s it! Once you’ve accomplished the above requirements, you would earn $8,000 in publicly traded eXp World Holdings (EXPI) common stock. This stock vests after three years.

You would acquire an additional $4,000 after one year, once your cultural requirements are fulfilled and verified.

ICON agents earn the last $4,000 in stock awards after attending each of the two annual eXp Realty events .

The company issues $2,000 after each company event (The eXp Shareholder Summit and EXPCON ) with no vesting period, for a possible total of $4,000 from attending the company events.

Wrapping Things Up

In conclusion, the eXp Realty Commission Split is very generous compared to the majority of brokerages out there. Especially when you consider the ICON Agent Program, eXp Realty is genuinely unique. Combine this with all the tools and training that eXp Realty provides to real estate agents, and you get an excellent opportunity to grow your career in real estate.

Do you have any questions related to the eXp Realty Commission Split? Put them in the comments below and I would be happy to answer them! Also visit Express Cash Flow.